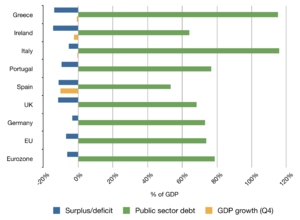

This week's chart focuses on the European debt crisis again because it remains unresolved:

The countries in crisis (PIIGS) need to refinance €1.5trillion in debt over the next three years. That is a near impossible task given the projected levels of

economic activity and the existing (aging) tax base in these countries. The following is a chart showing Europe's falling GDP and leading indicators:

The 'kick the can' approach used to date by the tag team of Merkle-Sarkozy has failed to convince

European bond buyers. If the euro union is to be saved it is becoming unavoidable that the Bundesbank allow the European Central Bank to essentially print more euros, so weak member nations can pay their debts. This is the route taken by the US Federal Reserve to avoid a crisis meltdown of the financial markets in 2008. The other alternative is to allow (perhaps the verb should be "force") Greece and other financially weak countries to leave the union to face national bankruptcy on their own with disastrous 'knock-on' effects for over leveraged European banks:

A common currency trading zone led by Germany could be reistablished with countries willing to enforce fiscal stability on themselves. For Germans who still remember the thousands of Weimar marks it once took to buy a loaf of bread or lump of coal, it is a bitter choice either way.